[ad_1]

Put up Views:

287

Fairness Market Insights:

The place is the recession? Regardless of being extensively anticipated for a lot of months, the recession has but to materialize within the US and different developed economies. The attention-grabbing query is why the recession has but not occurred even after one of many quickest will increase in rates of interest in historical past by all the key Central Banks in a really quick span of time.

Right here lies the reply as per the report from UBS:

- Financial coverage just isn’t restrictive sufficient to trigger a recession

- Fiscal coverage is marginally expansionary and fuelling funding

- Robust family stability sheets are supporting spending

- Credit score circumstances have tightened, however they don’t seem to be overly tight

- Labour demand and provide dynamics are retaining the market tight

With the see-saw of expectations from tender touchdown to slower progress together with expectations of early reversal of credit score tightening, markets made sturdy upward motion. Sensex went up by 9.5% over the Apr-June quarter whereas BSE Mid and Small Cap index rose by 19% and 20% respectively. All of the sectors went up with main sectoral progress seen in auto (up 22%), realty (up 33%), and shopper durables (up 13%) on the again of an enhancing financial outlook. India being highlighted as a beneficiary from the shift in World equations together with the anticipated highest financial progress amongst main economies has attracted sturdy flows from the FIIs lifting total market sentiments.

The current rally available in the market has made the valuations dearer in comparison with historic requirements. There’s little doubt that India’s story is robust and would maintain for the subsequent decade or two given the demographic benefit and favorable World scenario. Nonetheless, heightened valuations don’t present consolation in replicating increased returns of the previous within the medium time period. Unresolved World uncertainties can produce a black-swan occasion which can instantly shift the notion from increase to gloom. Valuations throughout all sectors don’t supply any margin of security. We imagine the markets can be extra risky over the subsequent 1 yr than they’ve been within the final 7 years. Increased volatility would throw extra alternatives for long-term worth buyers.

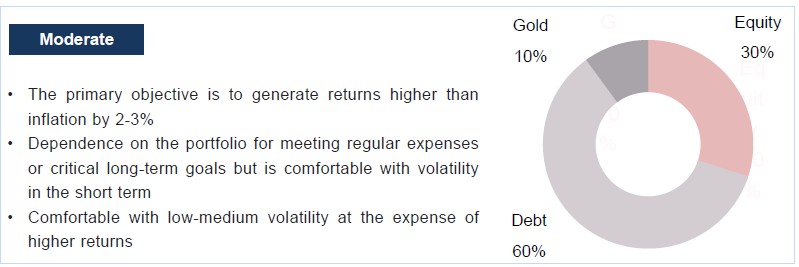

We proceed to remain under-allocated to fairness (verify the third web page for asset allocation) on the present valuation ranges. The sectors we like are vitality, pharma, and worth shares in large-cap area. At this stage, we strongly suggest minimizing publicity to small & mid-cap portfolios on the again of extreme valuations pushed by the retail craze.

We’re sustaining 5-10% portfolio publicity to Asian shares (China, Singapore, Taiwan, and so on.) on the again of valuation consolation and for diversification functions.

Debt Market Insights:

The debt yields for the shorter period got here down a bit owing to expectations of relaxed financial circumstances with a better-than-expected decline in inflation numbers. Yr-on-year declines in vitality costs have been the key contributor to total inflation numbers throughout developed economies.

Lengthy-duration yields remained elevated after a quick decline on the again of rising yields within the US market after the FED’s commentary on increased rates of interest for an extended time. The pause in charge hikes by the FED and RBI within the final quarter resulted in range-bound yield actions. The upside threat on inflation stays within the US as a result of increased wage progress leading to sticky core inflation. In India, monsoons can play a spoilsport leading to increased costs of meals which might preserve the RBI on tenterhooks. Any spurt in vitality costs would additional deteriorate the inflation outlook.

We proceed to imagine that the reversal in rates of interest could take a while since US Fed has clearly indicated that they are going to be knowledge dependent and studying on core inflation just isn’t falling quick sufficient which might warrant a change in stance.

We proceed to favor a portfolio period of round 1-1.5 years with ideally floating charge devices owing to volatility within the rate of interest eventualities. Dedication to long-term maturity papers must be averted for the reason that odds of decrease rates of interest for an extended time are nonetheless not very sturdy.

Different Asset Lessons:

After a powerful rally, Gold cooled off in Q1FY24 on the again of revenue reserving and shifting focus in the direction of fairness. Gold continues to be represented in all our shopper portfolios with an allocation of 10-20% relying upon threat profile and fairness publicity. Though there was no main disturbing information Globally within the final quarter, we imagine World uncertainties are right here to remain as a result of tug-of-war on shifting World financial energy middle.

Actual property costs in India have seen a leap in just a few areas after a lull interval from 2014 to 2021 on the again of rising revenue ranges and the growing urge for food of buyers to park surpluses. Any additional upside will not be as sturdy as seen within the final 2 years. General, we proceed to suggest sticking to asset allocation with self-discipline. It will guarantee increased risk-adjusted returns over the long run with decrease portfolio volatility and peace of thoughts.

TRUEMIND’S MODEL PORTFOLIO – CURRENT ASSET ALLOCATION

Truemind Capital is a SEBI Registered Funding Administration & Private Finance Advisory platform. You possibly can write to us at join@truemindcapital.com or name us at 9999505324.

[ad_2]