– Shopping for “Italy’s Best” for under 50 Cents on the Euro ?")

[ad_1]

Disclaimer: This isn’t funding recommendation. PLEASE DO YOUR OWN RESEARCH !!!!

What higher day to publish a put up about an Italian firm than Ferragosto, the Italian Public Vacation the place nearly any Italian household is someplace near a seashore and Italian workplaces solely are staffed with probably the most junior individual to take up the telefone so as to say: “Nobody right here, please name subsequent week/subsequent month”.

With Italmobiliare, I fell deeply right into a rabbit gap, which result in a fairly intensive evaluation. Attributable to some issues with the WordPress editor, I wrote it with a special Editor and have hooked up the PDF with the total model. Within the weblog put up I’ll concentrate on the chief abstract, the Professional’s and Con’s and the return expectations. The remainder of the gory particulars could be learn within the hooked up PDF doc.

Government abstract:

Italmobiliare (IM) is an Italian Holding firm with a market cap of ~1 bn EUR that underwent 2 pivots in its 40 12 months historical past as a listed firm. The primary pivot, within the Nineties, from conglomerate to Cement (Italcementi) after which as soon as once more in 2017 after a 2 bn sale to Heidelberger into an Italy centered, “High quality-growth small/mid cap PE” fashion funding firm.

What makes the corporate very enticing to me, is a really fascinating portfolio (together with a minimum of two potential “Tremendous Star” holdings), respectable worth creation, good technique/transparency and particularly a 50% Low cost to NAV.

For my part, the principle cause for the low cost is that the story and the standard of the portfolio will not be well-known and Italian Holdco’s are possibly not the most well-liked investments proper now.

However, this probably represents a beautiful return/danger profile for the affected person investor even with out the presence of a “laborious” close to time period catalyst.

Potential Catalysts

General, there’s clearly no laborious catalyst. “Delicate” catalysts can be a steady good and even nice efficiency of the flagship corporations and possibly a bigger exit within the subsequent 2-3 years. An IPO or perhaps a sale of Caffe Borbone as an example may make an enormous distinction. Or if Santa Maria grows 30-50% p.a. for some, traders may discover as properly.

If, and this can be a large IF, a share purchase backhappens, even a smaller one may compress the low cost, however I’d not wager on it. The largest hope can be that the opposite workers, who are also incentivized based mostly on NAV, maintain pressuring their boss who possibly has a for much longer time horizon.

One other risk may very well be in fact as soon as once more an activist investor, however I’d don’t know who this may very well be. The absence of such a catalyst could be a part of the reason for the excessive low cost and why Italmobiliare will not be very well-known.

Valuation/Return expectations

Italmobiliare will not be a Serial Acquirer however a “purchase and promote” Investor. Due to this fact, in my view, the NAV is the most effective valuation metric. A consolidated “look by way of” EV/EBIT valuation or related doesn’t make loads of sense because of the heterogeneity of the portfolio. That is additionally one of many explanation why the inventory doesn’t display screen properly. Screeners solely present e book values, not NAV.

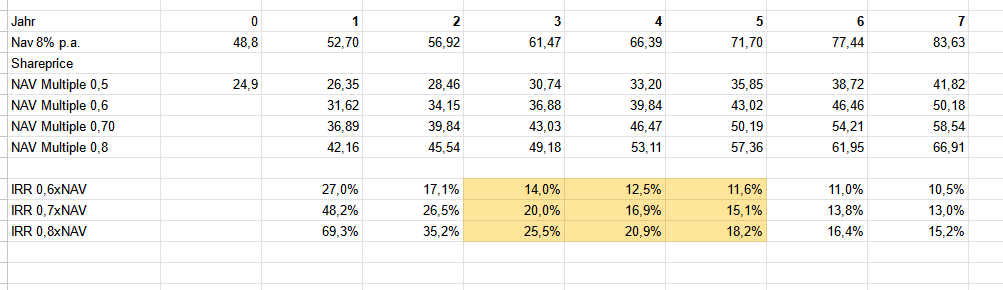

Based mostly on this, the return expectation has two primary parameters: NAV progress and assumed low cost to NAV. If the low cost stays 50% and so they handle to extend the NAV with 8% p.a. (incl. dividends) then the return might be 8%. If nevertheless the low cost narrows, then returns may very well be Turbocharged.

The next desk reveals the IRRs based mostly on an 8% NAV progress, a share value of 60-80% of NAV alongside the time axis.

The orange field is the world that I feel is real looking. Within the low case, it takes 5 years to succeed in 60% of NAV which is able to return 11,6% p.a. (incl. dividends). In the most effective case, I’ll double my cash after 3 years if the share value reaches 80% of NAV on this time. In fact , returns may very well be higher or phrase, however I feel that the “anticipated” return is one thing like 15-17% p.a. over 3-5 years. Which I feel is enticing.

Professionals/Cons

As all the time, even after a fairly extreme deep dive, time for a Professional/Con record:

+ Important low cost to NAV

+ No holding debt (solely at participation stage) or different structural points

+ good reporting

+ fascinating portfolio with some potential “Star Firms” (Caffé Borbone, Prof. Santa Maria)

+ doesn’t display screen properly

+ story will not be well-known

+ Household owned, proprietor operated, aligned incentives

+/- fairly OK NAV monitor file (8% p.a.)

– partial “Household workplace” character

– Holding value + taxes

– No “laborious” catalyst

Abstract

General, I do suppose that Italmobiliare is a really fascinating case. The present transformation doesn’t appear to be well-known, however in my view, Italmobiliare is a really fascinating “household funding” car run by a really sensible proprietor operator.

Their portfolio appears to be like fascinating and has good progress potential. The one drawback is the absence of a “laborious catalyst”. This nevertheless is compensated by a greater than snug low cost of fifty% to the NAV.

For the affected person investor, this creates a terrific alternative over a time horizon of a minimum of 3-5 years. Due to this fact I allotted 3,3% of the Portfolio into Italmobiliare at 24,20 EUR per share.

[ad_2]